How to Stop Impulse Spending With the 48-Hour Rule

Anúncios

Impulse spending is a common financial pitfall that affects millions worldwide. In an age of easy credit, persuasive marketing, and instant online purchasing, resisting the urge to buy on a whim has become increasingly difficult. However, one simple behavioral technique — known as the 48-hour rule — can be highly effective in curbing impulsive purchases and promoting healthier financial habits. This article explores how this rule works, why it is effective, and practical ways to implement it in everyday life, supported by real examples and data.

Understanding Impulse Spending: What Drives It?

Impulse spending refers to unplanned purchases made without prior consideration of cost, necessity, or future consequences. According to a survey published by the National Endowment for Financial Education, approximately 80% of Americans admit to making impulse purchases, with the average person spending around $165 per month on such expenses. This significant amount often leads to financial stress, debt accumulation, and undermines long-term savings goals.

Anúncios

Several emotional and psychological factors fuel impulse spending. Instant gratification, boredom, social influence, and marketing triggers all play crucial roles. For example, flash sales and limited-time offers create a sense of urgency, encouraging consumers to act quickly without reflection. Jean Twenge, a professor at San Diego State University, found in her research that younger generations, particularly millennials and Gen Z, are more prone to impulse spending due to the pervasive presence of digital advertising and social media platforms that constantly showcase desirable products.

Understanding these underlying triggers is vital for addressing impulse spending effectively. The 48-hour rule works by injecting a period of thoughtful delay that interrupts automatic purchase behavior, allowing reason and reflection to take precedence.

Anúncios

The Mechanics of the 48-Hour Rule

The 48-hour rule is a simple behavioral strategy that urges consumers to wait at least 48 hours before making a non-essential purchase. Instead of buying immediately, the individual commits to reassessing the need or desire for that item after two full days. During this cooling-off period, impulsive urges often diminish, allowing more rational financial decision-making.

The psychological basis is linked to the emotional brain—specifically the limbic system—overpowering the rational prefrontal cortex during moments of impulse. Waiting creates temporal distance, giving the rational brain time to evaluate whether the purchase aligns with priorities. A study published in the *Journal of Consumer Psychology* supports this notion: impulsive shopping was significantly reduced when participants employed a decision delay of 24 to 72 hours.

For example, a shopper tempted by a trendy gadget priced at $150 might feel excited initially but could later realize that they don’t genuinely need it, leading to a canceled or avoided purchase. This delay can prevent costly mistakes driven by temporary emotional highs.

Implementing the Rule: Practical Steps and Real-Life Examples

Applying the 48-hour rule requires intentional discipline. Here is an effective step-by-step method:

1. Identify the impulse: Recognize when a purchase is spontaneous and not part of your planned budget. 2. Pause and commit: Decide to wait 48 hours before revisiting the idea. 3. Reflect during the waiting period: Ask yourself questions such as “Do I really need this?” or “Could I use this money better elsewhere?” 4. Make a final decision: After the waiting period, either proceed with the purchase with confidence or cancel it altogether.

Consider the real-world case of Sarah, a 28-year-old graphic designer who struggled with online shopping habits. By committing to the 48-hour delay rule, she reduced her monthly impulse spending from $250 to just $60 within three months. Sarah reported feeling more in control of her finances and less buyer’s remorse.

Another example involves John and Marie, a couple who applied the rule to their gadget buying habits. John previously bought new tech devices impulsively, often reselling them at a loss. By waiting 48 hours, they noticed a drop in unnecessary purchases and allocated those savings towards their emergency fund.

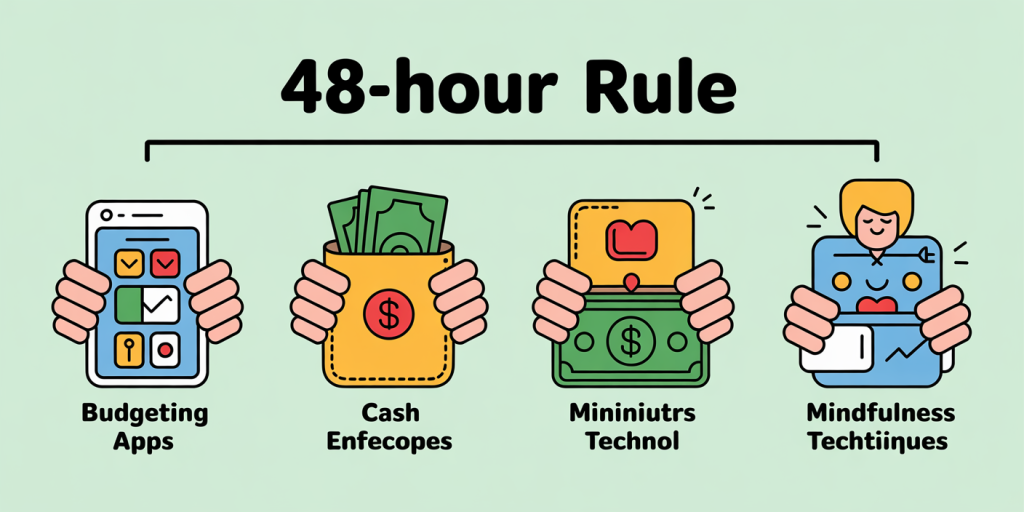

Comparing the 48-Hour Rule With Other Spending Control Techniques

Numerous methods exist for controlling impulsive spending, but the 48-hour rule stands out for its simplicity and effectiveness. Consider the following comparative table:

| Method | Description | Advantages | Disadvantages |

|---|---|---|---|

| 48-Hour Rule | Wait 48 hours before purchasing non-essentials | Easy to follow, encourages reflection | May delay needed urgent buys |

| Budgeting Apps | Use apps to track and control spending | Accurate tracking, provides insights | Requires tech literacy & discipline |

| Cash Envelope System | Allocate cash for categories in envelopes | Limits spending to physical cash | Inflexible, inconvenient for online shopping |

| Automatic Savings | Divert money before spending opportunity | Builds savings automatically | Does not directly control spending urges |

| Mindfulness Techniques | Practice awareness to identify urges | Improves emotional regulation | Takes time to develop, less structured |

While budgeting apps and automatic savings help overall money management, they may not directly prevent emotional impulsive buys as effectively as the 48-hour rule, which specifically targets the decision-making moment.

Benefits Beyond Financial Savings

Though the most obvious benefit is financial, the 48-hour waiting rule promotes broader psychological and behavioral improvements. Firstly, it fosters self-discipline and intentionality in spending, which can translate to other life areas such as diet or time management.

Secondly, it reduces stress and regret associated with impulsive purchases. A 2019 study by the American Psychological Association found that impulsive spenders reported higher levels of anxiety and depression linked to financial insecurity. By avoiding impulse buys, people often experience improved mental well-being and a greater sense of control.

Furthermore, the rule assists in combating consumerism-encouraging societal norms. In an era dominated by “buy now” culture, slowing down decisions challenges habitual overconsumption and environmental impact, encouraging more sustainable spending behavior.

Future Perspectives: Digital Tools and Behavioral Insights

The 48-hour rule’s effectiveness will likely increase as new technologies and behavioral science advances emerge. Digital wallets and payment systems may soon feature built-in “cooling-off” periods, embedding the rule directly into purchase pathways. For instance, Amazon and other e-commerce platforms could one day implement optional 48-hour holds on certain purchases, prompting buyers to reconsider before finalizing.

Behavioral economists are also exploring AI-driven nudges tailored to individual spending patterns. Customized alerts reminding consumers to wait 48 hours may reduce impulse purchases more effectively than generic advice.

Moreover, as financial literacy education evolves, more institutions are promoting delay purchase techniques like the 48-hour rule within curricula and counseling services. Broader awareness could lead to societal shifts in spending culture, prioritizing financial health and mindful consumption.

Despite technological assistance, the core success lies in personal commitment. Practicing patience in spending decisions not only safeguards finances but cultivates a mindset of thoughtfulness and restraint critical for long-term wealth building.

—

By integrating the 48-hour rule into daily financial habits, individuals can dramatically reduce impulse spending, increase savings, and experience improved emotional well-being. This straightforward yet powerful technique acts as a buffer against the fast-paced, convenience-driven consumer environment, empowering better financial decisions and fostering sustainable spending habits for the future.

Post Comment