Disability Insurance: The Most Overlooked Financial Safety Net

Anúncios

In the realm of personal finance, some protections are more visible and celebrated than others. Homeowners’ insurance, life insurance, and health insurance often dominate financial planning discussions. Yet, one critical form of coverage remains vastly underappreciated—disability insurance. This financial safety net can provide the essential income replacement that many people overlook until it’s too late. Understanding the importance of disability insurance and incorporating it into your financial strategy can mean the difference between financial stability and hardship if a disabling event occurs.

Statistics from the Social Security Administration reveal that nearly one in four workers will experience a disability lasting 90 days or longer before reaching retirement age (SSA, 2023). Despite this, only about 50% of American workers have any form of disability insurance. This gap highlights the urgency of awareness and education about disability insurance as a key component of risk management.

The Real Risk of Disability and Financial Impact

Anúncios

Disabilities can happen to anyone, regardless of age, occupation, or health status. The risk is not limited to older adults or high-risk professions. According to the Council for Disability Awareness, the leading causes of disability are not catastrophic accidents but rather illnesses such as cancer, heart disease, and musculoskeletal disorders (CDA, 2022). These conditions can strike at any time, often with little warning.

Consider the case of Lisa, a 35-year-old graphic designer who suffered a severe back injury from an unexpected fall. Unable to perform her duties for over six months, she found herself struggling with bills and everyday expenses despite having health insurance. Without a steady income, her savings quickly diminished. If Lisa had comprehensive disability insurance, her policy would have replaced a portion of her income, ensuring she could cover her essential expenses while recovering.

Anúncios

A professional person (e.g., graphic designer or office worker) unable to work due to injury, surrounded by bills and financial documents, illustrating the financial impact of disability without insurance.

The financial toll of disability is not just about medical bills; it extends to lost income and lifestyle adjustments. A Financial Industry Regulatory Authority (FINRA) survey found that 60% of Americans would face serious financial hardship within six months of losing their primary source of income (FINRA, 2021). Disability insurance fills this critical gap by providing a reliable income stream.

Types of Disability Insurance and How They Differ

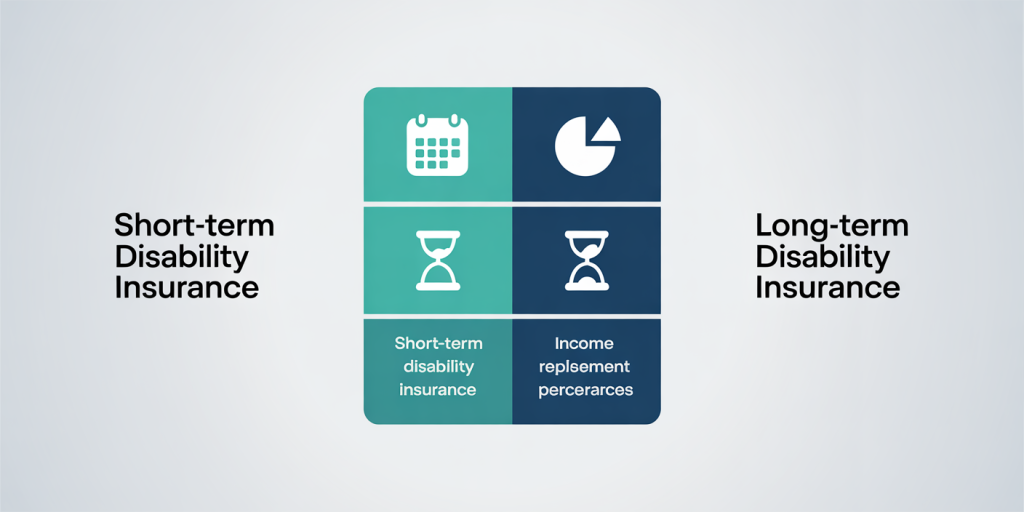

Disability insurance is broadly categorized into two types: short-term disability insurance (STDI) and long-term disability insurance (LTDI). Both serve the purpose of replacing income when disability strikes, but they vary significantly in duration and coverage scope.

Short-term disability insurance typically covers disabilities that last from a few weeks up to six months. It usually begins paying benefits after a waiting period of one to two weeks and replaces around 60% of the insured’s income. This type of insurance is often offered as part of employee benefits packages. For example, Sarah, a corporate accountant, received short-term disability benefits after surgery to remove a benign tumor, allowing her to focus on healing without financial stress.

Long-term disability insurance, conversely, starts after the short-term benefits end, often after three to six months of disability. It can provide coverage for several years or until the insured reaches retirement age, depending on the policy. Long-term policies usually pay around 50-70% of pre-disability earnings. Consider the story of Tom, a software engineer who developed a chronic illness resulting in permanent disability and inability to work. His long-term disability policy became essential in maintaining his family’s financial stability over the years.

The following comparative table outlines key differences between STDI and LTDI:

| Feature | Short-Term Disability Insurance | Long-Term Disability Insurance |

|---|---|---|

| Coverage Duration | Weeks to 6 months | Several years up to retirement age |

| Waiting Period | 1 to 14 days | 90 to 180 days |

| Income Replacement | Typically 60-70% of income | Usually 50-70% of income |

| Common Availability | Employer-sponsored or individual plans | Employer-sponsored or individual plans |

| Typical Use Case | Temporary injury or illness | Severe or permanent disability |

Understanding these distinctions helps individuals choose the most suitable coverage for their lives and risk tolerance.

A clear, visually appealing comparative infographic/table showing key features of short-term vs. long-term disability insurance, highlighting coverage duration, waiting periods, and income replacement percentages.

Why Disability Insurance Is Often Overlooked

Despite the clear benefits, many individuals either do not purchase disability insurance or underestimate its importance. Several psychological and financial reasons contribute to this oversight. One major reason is optimism bias—the tendency to believe that adverse events, such as disabling illness, are more likely to happen to others than oneself.

Moreover, compared to other types of insurance, the immediate consequences of disability can feel less tangible. Unlike life insurance, which provides for survivors, disability insurance affects the insured’s present lifestyle, making it difficult for people to visualize the risk. Additionally, since medical insurance covers treatment but not lost income, many assume they are financially protected when that is not the case.

Cost is another factor. Some individuals view disability insurance premiums as an unnecessary expense, especially if offered as an optional employee benefit. However, the price of inaction can be catastrophic. A salary replacement of 60% may seem expensive as a monthly premium, but when compared to the loss of income, the value becomes apparent.

Jane, a nurse, once declined her employer’s disability plan to save money. Two years later, she was diagnosed with rheumatoid arthritis, restricting her ability to work. Without coverage, Jane faced a complete loss of income and mounting debts. Her story illustrates the perils of neglecting this insurance.

How to Choose the Right Disability Insurance

Selecting the right disability insurance policy involves careful consideration of personal circumstances, financial goals, and risk factors. Several key variables influence the suitability of a policy, including whether you should prioritize employer-sponsored plans, individual coverage, or both.

Employer-sponsored disability insurance often provides a convenient and affordable option, but its benefits might come with limitations. For example, many employer policies only cover a percentage of your salary, have strict definitions of disability, or limit coverage duration. If your employer offers disability insurance, it’s essential to understand the policy specifics and assess whether additional coverage is necessary.

Individual disability insurance policies offer more customization, allowing for tailored waiting periods, benefit amounts, and longer coverage durations. These policies are especially important for self-employed individuals or those whose employer coverage is insufficient. For instance, Dr. Mark, a self-employed dentist, chose an individual long-term disability policy that articulated “own occupation” coverage, which pays benefits if he cannot work in his specific profession, even if he can perform other jobs.

When assessing disability insurance options, pay attention to: Definition of Disability: Some policies require you to be unable to perform any job (any-occupation), while others cover inability to work in your own occupation. Benefit Period: How long will benefits be paid—until recovery, a specific number of years, or retirement age? Waiting Period (Elimination Period): The length of time before benefits start. Premium Cost and Increases: Whether premiums are fixed or could increase over time.

The Financial Implications and Cost-Benefit of Disability Insurance

The price of disability insurance may seem burdensome, especially to young people or those with tight budgets. However, when weighed against potential financial loss during disability, the benefits significantly outweigh the costs. Data from LIMRA’s 2023 Insurance Barometer study reveals that a typical monthly premium for a 30-year-old non-smoker earning $60,000 is around $50 for a comprehensive long-term disability policy. This investment protects against a potentially devastating loss of thousands in monthly income.

Let’s analyze a hypothetical example:

| Scenario | Without Disability Insurance | With Disability Insurance |

|---|---|---|

| Monthly Gross Income | $5,000 | $5,000 |

| Income Lost Due to Disability | $5,000 | $0 (covered by policy) |

| Monthly Benefits from Policy | $0 | $3,000 (60% replacement) |

| Monthly Premium Cost | $0 | $50 |

| Net Monthly Income After Disability | $0 | $2,950 ($3,000 – $50) |

This table illustrates that paying a $50 premium can safeguard against a total loss of income and still allow covering essential expenses. The small monthly sacrifice ensures long-term financial security and mitigates the risk of debt accumulation or forced asset liquidation.

Disability Insurance in the Broader Financial Planning Context

Disability insurance should not be viewed in isolation but as an integral part of comprehensive financial planning. It complements other protections like emergency savings, life insurance, and health insurance.

Emergency funds provide temporary relief but can quickly erode during extended periods without income. Life insurance protects dependents against premature death but does not address income interruption while the insured is alive but unable to work. Health insurance covers medical costs, but typically excludes lost wages.

Including disability insurance in your financial plan fosters resilience, preserving your lifestyle and financial obligations. For example, financial advisors often recommend coverage that replaces at least 60% of gross income. This threshold balances realistic income replacement with affordable premiums.

Real-life case studies showcase how disability insurance prevents financial catastrophe. David, a 28-year-old teacher, was diagnosed with multiple sclerosis. His long-term disability policy ensured continuous benefit payments, enabling him to pay his mortgage and support his family. Without this safety net, David would have faced foreclosure and severe financial distress.

Future Perspectives: The Evolving Role of Disability Insurance

As workforce dynamics and healthcare evolve, the role of disability insurance is becoming increasingly critical. The rise of gig workers and freelancers, who typically lack employer-sponsored benefits, drives demand for portable individual policies. Additionally, as chronic illnesses and mental health conditions become more recognized as disabling, policies are adapting to offer broader definitions and coverage terms.

A diverse group of workers (including gig workers and freelancers) reviewing disability insurance options with an insurance advisor, symbolizing the evolving role and importance of disability insurance in modern financial planning.

Technological advancements enable insurers to offer more personalized underwriting using data analytics and AI, potentially lowering costs and expanding access. Policies that integrate wellness programs and early intervention strategies can also reduce claim durations and improve outcomes.

Moreover, government policy shifts may influence private disability insurance. Proposals to expand Social Security Disability Insurance (SSDI) and reform eligibility criteria can complement private coverage but are unlikely to replace it entirely. This dual approach will emphasize the importance of private disability insurance as a vital supplement.

In summary, disability insurance is evolving from a niche product to a mainstream financial necessity. Awareness campaigns, improved product transparency, and innovative solutions are poised to close the protection gap.

Disability insurance remains one of the most underestimated and undervalued financial tools. With significant risk of disability before retirement age and the potentially catastrophic financial impact, securing appropriate coverage should be a priority for everyone. By understanding its types, benefits, and how to choose the right policy, individuals can safeguard their income and secure financial stability, regardless of what life throws their way.

Post Comment