Zero-Based Budgeting vs. Envelope System: Which Budgeting Style Suits You Best in 2025?

Anúncios

In 2025, managing personal finances effectively remains a pivotal challenge for many individuals and families worldwide. With rising living costs, fluctuating incomes, and increasing financial uncertainties, choosing the right budgeting method can profoundly impact financial health and peace of mind. Among the plethora of money management techniques, two approaches—Zero-Based Budgeting (ZBB) and the Envelope System—continue to maintain significant popularity. Both methods promote disciplined spending and enhanced savings but differ drastically in structure and implementation.

This article explores these two budgeting styles, comparing their principles, benefits, drawbacks, and suitability in the current economic climate. Whether you are a meticulous planner or prefer tangible cash management, understanding these systems will help you decide which budgeting technique aligns with your financial goals and lifestyle in 2025.

Understanding Zero-Based Budgeting: Every Dollar Counts

Anúncios

Zero-Based Budgeting is a technique where every dollar of your income is allocated to specific expenses, savings, or debt repayment, resulting in a “zero” balance at the end of the budgeting period. Instead of just tracking expenses after spending, ZBB requires proactive planning before the money is spent.

The core principle behind ZBB is intentionality—each dollar is assigned a purpose, whether it is a fixed bill, variable expense, or fund towards future goals. For example, if you earn $5,000 monthly, you would allocate the full $5,000 to categories such as rent, groceries, entertainment, savings, and investments so that your income minus your expenditures equals zero. It’s not about spending all your money but ensuring that every dollar has a job, reducing unnecessary or impulsive expenditures.

Anúncios

ZBB originated in corporate budgeting but has increasingly been adopted for personal finances. According to a 2023 survey by the National Endowment for Financial Education (NEFE), approximately 38% of Americans who actively budget credit this method for improved financial control and reduced wasteful spending. The meticulous nature of ZBB appeals to those who desire precise control over their money and wish to identify and eliminate hidden financial leakages.

The Envelope System: Tangible Cash Management for Practical Budgeting

The Envelope System is a traditional cash-based budgeting method that physically separates money into envelopes marked for various spending categories. This low-tech system ensures that one only spends the cash allocated to each envelope, helping to promote discipline and prevent overspending.

For instance, if your monthly grocery budget is $400, you place $400 in a labeled grocery envelope. When shopping, you pay only with the cash in your envelope. When the cash is gone, spending must stop. This tangible constraint helps avoid digital overspending, which is common with credit cards or mobile payments.

The envelope method surged in popularity during the pre-digital era but has found renewed relevance in 2025, combining with digital tools such as budgeting apps that simulate the envelope system virtually. Its effectiveness lies in providing psychological cues through physical cash or visual representation, making it ideal for people who struggle with overspending or need clearer spending boundaries.

A 2022 study by the Financial Planning Association (FPA) revealed that users of the Envelope System reported a 20% improvement in sticking to budget limits compared to those using only app-based budgets. This system’s intuitive approach helps develop strong spending habits and financial discipline.

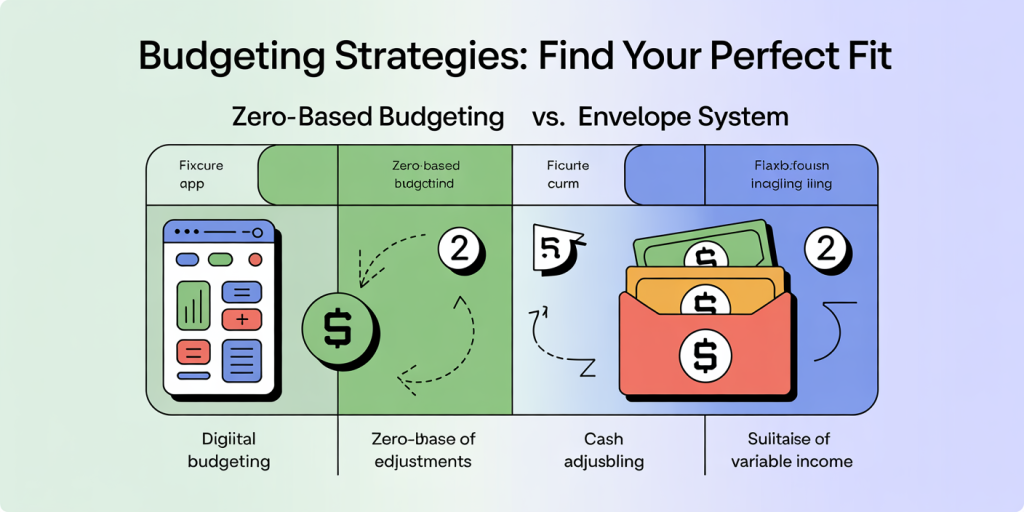

Comparing Zero-Based Budgeting and the Envelope System: Which is More Flexible?

Flexibility is a crucial factor when choosing a budgeting style, especially considering today’s unpredictable financial environment. Zero-Based Budgeting offers high flexibility through detailed allocation and ongoing adjustments. As income or priorities change, categories can be tweaked monthly, allowing dynamic adaptation. For example, if a freelancer’s income varies, ZBB enables reassigning funds to match fluctuating earnings and upcoming expenses.

The Envelope System is more rigid, especially when using physical cash envelopes. Once money is distributed to different categories, transferring funds between envelopes can be inconvenient and psychologically difficult, potentially necessitating a mid-month “re-budget.” However, when used with digital apps that simulate the envelope system, this flexibility improves, albeit losing some benefits of tangible cash limitation.

The Envelope System in practice: physical envelopes labeled with spending categories filled with cash, alongside a family or individual using them to control expenses, showing tangible budgeting and discipline.

| Aspect | Zero-Based Budgeting | Envelope System |

|---|---|---|

| Flexibility | Very Flexible; monthly adjustments | Moderate; physical envelopes less flexible; better via apps |

| Ease of Adjustments | Requires careful recalculation | More manual reallocation needed |

| Good for Variable Income | Excellent for fluctuating incomes | Can be challenging but manageable |

Individuals with fluctuating or unpredictable incomes often prefer ZBB due to the ease of tweaking allocations, while those favoring strict spending limits might gravitate toward the Envelope System.

Comparison table infographic of Zero-Based Budgeting vs. Envelope System highlighting flexibility, ease of adjustments, and suitability for variable income, with icons representing digital apps integration and cash handling.

Practical Use Cases: Who Benefits Most from Each System?

Zero-Based Budgeting has proved advantageous for individuals aiming for detailed financial control and goal-oriented planning. For example, Sarah, a 29-year-old graphic designer in Austin, Texas, used ZBB to allocate her $4,500 monthly income. Her budget included exact amounts for rent, utilities, debt payments, groceries, emergency fund contributions, and retirement accounts. Over six months, Sarah reported a 25% increase in saving rates and paid off $6,000 in credit card debt, attributing her progress to the clarity and intention fostered by ZBB.

In contrast, Mike and Jane, a couple with three children in Orlando, Florida, struggled with credit card overspending. They adopted the Envelope System, placing cash envelopes for groceries, dining out, kids’ activities, and entertainment. Using cash limited their impulsive spending, resulting in a 30% reduction in discretionary expenses over a year. The tactile nature of cash helped the family visualize their spending limits and stay accountable.

People who are comfortable with technology but want tangible spending controls can leverage apps like Goodbudget or Mvelopes, which digitize the Envelope System, blending convenience with discipline. Those motivated by precise allocation and financial planning detail might prefer apps tailored for ZBB, such as EveryDollar.

Psychological and Behavioral Insights: Impact on Spending Habits

Both budgeting methods influence financial behavior but in slightly different ways. Zero-Based Budgeting promotes mindfulness by compelling planners to assign every dollar before spending, which reduces unconscious spending and waste. The method encourages proactive money management and provides granular insight into spending patterns, helping to avoid the “leftover money” trap where unallocated funds get frittered away.

Visual representation of Zero-Based Budgeting: a detailed monthly budget planner allocating every dollar with charts and categories, emphasizing precision and intentional money management.

The Envelope System’s psychology is rooted in boundary setting and loss aversion. Physically seeing money leave an envelope triggers more mindful spending and prevents overspending by creating a tangible limit. Behavioral economists note that limitations framed as physical boundaries, like cash envelopes, are more effective in controlling impulsive purchases than digital tracking alone.

Research published in the Journal of Consumer Research (2023) highlighted that users of cash-based budgets like the Envelope System tend to save 15% more on impulse purchases than those relying solely on digital budgeting methods. However, highly organized individuals who prefer detailed planning often benefit more from ZBB’s comprehensive approach.

Thus, the choice between these methods largely depends on personal psychology—whether you respond better to planned allocations or tangible spending limits.

Technology Integration: Adapting Both Systems for the Digital Age

In 2025, digital tools and mobile apps have revolutionized budgeting, adding new dimensions to traditional methods. ZBB and the Envelope System can both be enhanced with technology, allowing more accurate tracking, flexibility, and insights.

ZBB-based apps, such as EveryDollar or You Need a Budget (YNAB), prompt users to allocate every dollar at the beginning of the month, track transactions in real time, and update budgets automatically. This reduces the manual effort and improves accuracy, making ZBB easier and more accessible.

For the Envelope System, apps like Goodbudget create virtual envelopes linked to bank accounts, providing real-time balances and reminders without needing physical cash. These apps simulate emotion-driven spending controls digitally, aiding those uncomfortable with carrying large amounts of cash but still prone to overspending.

While technology increases convenience, it also introduces risks, such as declining awareness of actual money flow due to digital detachment. Still, studies show that 67% of millennials using budgeting apps maintain higher budgeting adherence than those without app support.

| Feature | Zero-Based Budgeting Apps | Envelope System Apps |

|---|---|---|

| Real-time tracking | Yes | Yes |

| Spending alerts | Customizable | Customizable |

| Flexibility | High; automatic recalculations | Moderate; manual adjustments possible |

| Cash handling | Virtual cash allocations | Virtual envelopes simulate cash |

Technology continues to bridge tradition with innovation, making these budgeting styles more adaptable to modern lifestyles.

Future Perspectives: Budgeting Evolution and Personalized Finance in 2025 and Beyond

As we progress through 2025, budget management techniques will evolve alongside economic trends and behavioral sciences. Both Zero-Based Budgeting and the Envelope System are likely to adapt through greater integration with AI and machine learning, offering tailored budgeting suggestions based on spending habits, income fluctuations, and life events.

Personalized finance platforms might combine the planning precision of ZBB with the behavioral triggers of the Envelope System, creating hybrid models that learn and adjust budgets in real time for optimum financial outcomes. For example, a future app might prompt users to allocate zero-based budgets initially and then warn when certain “virtual envelopes” are nearing depletion, blending accountability and planning.

Moreover, as financial literacy improves globally, more individuals will demand flexible yet psychologically informed budgeting approaches. Tools that foster both intentional allocation and spending discipline will gain prominence, especially in uncertain economic climates marked by inflationary pressures and evolving income sources like gig and freelance work.

In conclusion, the choice between Zero-Based Budgeting and the Envelope System in 2025 depends largely on personal finance goals, behavioral tendencies, and lifestyle. Detailed planners and those with variable incomes might lean towards ZBB’s precision, while those requiring tangible spending limits to curb impulsiveness may prefer the Envelope System’s clear boundaries. Embracing the strengths of both with supportive technology can lead to smarter, more adaptable budgeting in an ever-changing financial world.

Post Comment